Business

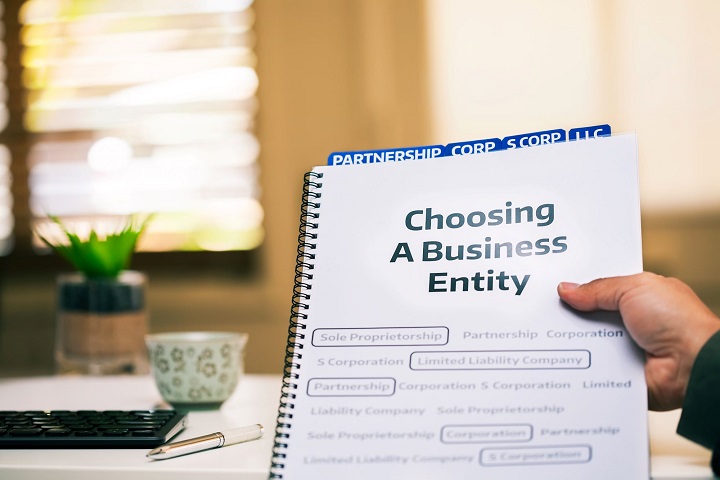

Incorporate A Business Ontario: 4 Pros And 3 Cons

Get ready to delve deep into this critical topic and equip yourself with the knowledge to steer your business journey confidently. Read on.

Ready to launch an entrepreneurial voyage in Ontario, Canada? One major fork in the road is whether or not to incorporate the business. It’s a meaty decision, bursting with promising benefits but not without its share of hurdles.

This post stands as a navigational aid, offering a full, clear view of the enticing rewards and potential stumbling blocks tied to business incorporation. Get ready to delve deep into this critical topic and equip yourself with the knowledge to steer your business journey confidently. Read on.

Table of Contents

A. Pros Of Incorporating In Ontario

Incorporating a business presents a compelling argument for entrepreneurs. Here are the advantages of choosing to incorporate a business Ontario:

1. Provides Access to Various Funding Opportunities

Incorporating a business enables access to a plethora of funding opportunities. Financial institutions, private investors, and government bodies in Ontario are more inclined to offer financial support to incorporated businesses. Why so? This is because corporations are perceived to be more stable and reliable, especially when compared to other business entities.

So, think about this. Wouldn’t it be fantastic to have multiple avenues to acquire funds when you incorporate a business in Ontario? Not only does it increase your financial security, but it provides growth and expansion possibilities for your business as well.

2. Offers Limited Liability Protection: A Safety Net For Personal Assets

Imagine being an entrepreneur and not having to worry about your personal assets in the face of business debts or legal issues. This is what a corporation brings to the table.

Unlike sole proprietorships or partnerships, the law sees an incorporated business as a separate legal entity from owners or members. In essence, your personal assets can’t be intertwined with your business debts. Thus, creditors can’t claim your personal assets like your home or vehicle to settle business debts. Now that’s peace of mind!

3. Perpetual Existence: The Business Lives On

A significant advantage when you incorporate a business Ontario is its perpetual existence. What does this mean? Well, unlike other business structures, an incorporated company outlives its founder. Regardless of changes in ownership or management, the business continues to exist and operate.

So, picture this. You’ve built a successful enterprise, and even if you decide to retire or sadly pass away, your hard work, your legacy, continues. Isn’t that a comforting thought?

4. Tax Benefits: More Money In Your Pocket

Incorporation opens doors to a multitude of tax advantages in Ontario. Compared to other business structures, incorporated businesses are said to enjoy lower tax rates. In addition, they’re eligible for numerous tax deductions, including costs associated with running a home business, vehicle expenses, business-related travel, and so on.

What could this mean for you? More money saved, more money to reinvest into your business! Imagine the possibilities with all the extra cash at hand.

The above-mentioned are just a few perks your business can enjoy if it goes with the incorporation route.

B. Cons Of Incorporating A Business In Ontario

As you’ve seen, incorporating a business in Ontario has numerous benefits. Yet this move brings a new set of responsibilities and costs, especially when compared to other structures such as sole proprietorships or partnerships. Here are the key challenges of choosing to incorporate a business in Ontario:

1. Higher Setup And Maintenance Costs

Incorporation comes with higher upfront and ongoing costs compared to other business structures. There’s the initial fee to incorporate a business in Ontario, legal fees, and costs associated with maintaining corporate records, such as the minute book. That’s quite a dent in the budget, right?

Moreover, corporations must file a separate corporate tax return yearly, often requiring hiring a professional accountant. Compared to a sole proprietorship or partnership, the costs can quickly add up while doing in one of Canada’s most economically important areas.

2. Increased Paperwork And Regulatory Requirements

Incorporating a business in Ontario comes with a significant increase in paperwork and regulatory requirements.

To incorporate a business, you’ll need to file Articles of Incorporation, maintain a minute book, hold annual shareholder meetings, and file annual reports. But wait, that’s not all! Any changes in the corporation, such as amendments to the Articles of Incorporation, changes in directors, or addresses, must be reported to the government.

Quite a handful, isn’t it? In contrast, a sole proprietorship or partnership is simpler to set up and has fewer compliance requirements instead of incorporating a business in Ontario.

3. Limited Personal Liability May Not Be Total Protection

While limited liability protection is often touted as a major advantage of incorporating, it’s crucial to note that it doesn’t offer total protection. In some circumstances, directors and shareholders can still be held personally liable, such as for unpaid wages, source deductions, and GST/HST remittances.

When you incorporate a business, Ontario law may protect your personal assets from business debts, but it doesn’t provide a free pass for irresponsibility or neglect. Is the limited liability shield as sturdy as you thought? Not necessarily.

Be mindful of the drawbacks mentioned beforehand in your quest in incorporating your business in Canada’s Ontario area.

Takeaway

Incorporating a business in Ontario presents you with a range of enticing benefits. Access to various funding opportunities, limited liability protection, perpetual existence, and tax benefits can greatly contribute to the success and growth of your business.

On the other hand, there are some cons to consider as well. Higher setup and maintenance costs, increased paperwork, and regulatory requirements, along with the reality that limited liability may not provide absolute personal protection can pose challenges to entrepreneurs.

Hence, as a business owner, you need to carefully weigh these pros and cons before deciding to incorporate your business in Canada’s Ontario.

Business

Tax Filing Advice: Self-employment Tax (IRS Form 1040)

In this post, we’ll show you how to fill out Form 1040 and offer some tips on how to minimize your tax obligations. Tax Filing Advice – Self-employment Tax – IRS Form 1040.

Filing your taxes can be challenging, especially if you are a freelancer. As a freelancer, you are required to pay self-employment tax, maintain track of your revenues and expenses, and submit projected tax payments throughout the year. You can complete an IRS Form 1040 with a little help and a quarterly tax calculator, despite the fact that it could appear challenging. In this post, we’ll show you how to fill out Form 1040 and offer some tips on how to minimize your tax obligations.

Table of Contents

1. Assemble Your Papers

Before you start filling out your Form 1040, you must gather all the necessary information and paperwork. Your W-2s, 1099s for any freelance work you did, receipts for any anticipated tax deductions, and any other financial records you might have are included in this. You must also include your Social Security number and the Social Security numbers of any dependents you wish to claim.

2. Verify Your Filing’s Status

Your file status affects your tax rate and the size of your standard deduction. Determine which filing status is appropriate for you based on your marital status, the number of dependents you have, and other factors.

3. Ascertain your income

Your total income for the tax year is what is referred to as your gross income. This includes all forms of income, including wages, salaries, tips, and revenue from side jobs. Add up your income for the tax year and gather all of your supporting papers. List all of your sources of income from contract work.

4. Remove Your Modifications

By deducting adjustments from your gross income, you can reduce your taxable income. They also pay your health insurance premiums, student loan interest, and IRA contributions if you work for yourself.

5. Choose Your Tax Savings

By taking some expenses out of your taxable income, you can reduce it. The two distinct types of tax deductions are standard and itemized. The standard deduction is an agreed-upon sum of money that is available to all tax filers. As itemized deductions, you are allowed to deduct some costs like state and local taxes, charity giving, and mortgage interest. It is better to select the tax deduction that would result in the greatest financial savings.

6. In Step Six, determine your taxable income.

After subtracting either your standard deduction or your itemized deduction from your AGI, your taxable income will be determined. According to federal law, this amount is your taxable income.

7. Choose Your Tax Credits

They are made up of education, earned income, and child tax credits. To reduce your tax obligation, find out which tax credits you are eligible for.

8. Find Out How Much Tax You Owe

Your overall tax liabilities, less any payments or credits, are referred to as your tax burden.

9. Verify Your Upcoming Tax Payments

If you are self-employed, you must make estimated tax payments throughout the year. Check your expected tax payments throughout the year to ensure you made the required amount to avoid underpayment penalties.

10. Finishing Schedule C

Schedule C, the relevant form, is used to report your self-employment earnings and expenses. To calculate your self-employment tax, which is based on your net self-employment income, use Schedule C. In addition to this, you will also owe regular income tax.

11. Add Up Your Credits and Payments

Add all of your year-end payments, such as estimated tax payments and any taxes you have withheld from your pay. If you qualify, take a deduction for any tax credits. Here, your overall payments and credits will be displayed.

12. Figure out whether you owe a refund or are due one.

You should evaluate your entire tax burden in relation to your total payments and credits. If your tax due is greater than the sum of your payments and credits, you will be obliged to pay extra tax.

13. Upload Your Return

When you’ve finished filling out Form 1040 and any necessary attachments, sign and date your return, and then send it to the relevant IRS address. Make sure to keep a copy of your return and any supporting documents for your keeping.

14. Tips on How to Cut Your Taxes as Much as Possible

Now that you know how, let’s speak about how to complete Form 1040 so that you may maximize your tax savings as a freelancer.

Using tax deductions is a smart move.

As a freelancer, you might be eligible to write off a range of expenses from your taxes, such as business travel, office supplies, and office equipment. Keep note of all your expenses throughout the year in order to maximize any relevant deductions.

Submit projected tax payments

As was previously stated, self-employed individuals are obligated to make projected tax payments throughout the year. This allows you to keep track of your tax obligations and prevent underpayment fines.

You May Want To Add

The ability to deduct more business expenses and a lower tax rate on self-employment income are just two of the additional tax benefits that incorporating your freelancing business may offer. Speak with a tax professional if you’re unsure if incorporation is the right option for you.

Employ tax-favored retirement accounts.

You may be able to reduce your taxable income and increase your tax savings by contributing to tax-advantaged retirement plans like an IRA or Solo 401(k). Use these accounts if you meet the requirements.

Conclusion

Although filling out a Form 1040 can be intimidating, with a little planning and assistance, it is actually rather easy. Even though you may face certain challenges as a freelancer when attempting to maximize your tax savings, there are a number of strategies you may employ to help minimize your tax burden. By taking advantage of tax deductions, paying expected taxes, considering incorporation, and using tax-advantaged retirement plans, you may keep more of your hard-earned money in your pocket.

Ways Paper Cutting Machine Is Used To Craft Perfection And Reduce Complexity

Mistakes You Want to Avoid While Purchasing Wedding Rings Online

Revolutionizing Home Care: How Technology is Transforming the Industry

Tax Filing Advice: Self-employment Tax (IRS Form 1040)

Digital Ghost Money: Understanding Cryptocurrency Value

Stocks or Currency for Investors: Bitcoin

Study of Bitcoin’s Transaction Finality and Irreversibility

Meeting point of Cybersecurity and Oil Trading

Eco-Friendly Flower Delivery: Sustainable Choices for a Greener World

Achieving Business Agility with AI-Integrated ERP Implementation

Buy IG likes and buy organic Instagram followers: where to buy them and how?

100% Genuine Instagram Followers & Likes with Guaranteed Tool

7 Must Have Digital Marketing Tools For Your Small Businesses

Instagram Followers And Likes – Online Social Media Platform

Top 25 Best SolarMovie Alternatives Updated List

Use of 3D Printing in Injection Molding

Principles of Good Software Engineering

How To Get Started With Artificial Intelligence

Tamilrockers Alternatives: TamilRockers Proxy and Mirror Sites [working]

The History of CAD (Computer-aided design)

-

Instagram2 years ago

Buy IG likes and buy organic Instagram followers: where to buy them and how?

-

Instagram2 years ago

100% Genuine Instagram Followers & Likes with Guaranteed Tool

-

Business4 years ago

7 Must Have Digital Marketing Tools For Your Small Businesses

-

Instagram3 years ago

Instagram Followers And Likes – Online Social Media Platform